Do Agricultural Cash Market Updates Vary Along Forward Curves?

Reading time : 6 minutes

In this study, we will compare the frequency of agricultural commodities cash markets’ quotes by scrutinizing spot shipment updates vs. forward price quotations.

Physical markets’ updates follow different dynamics. Some markets are mostly updated on a spot basis (such as Russian wheat), while others are trading on a forward basis (Like Brazil Corn). So some origins can hedge well in the future while others seem to remain long until the execution date. These dynamics are critical to understanding the timing of convergence between cash and futures markets.

Which flows are trading solely on a spot basis?

Which origin is pricing or hedging forward?

Methodology

We are crossing the evolution of FOB prices from several exporting origins:

Soybean Brazil

Soybean Meal Argentina

Wheat Russia

Wheat Ukraine

Barley Ukraine

Corn Brazil

By anchoring the analysis around when the update is done vis-à-vis the related shipment period. We use simple statistical and analytical methods and classic data science tools to study the markets and reach our conclusions.

[We did these data analysis steps with most used libraries in python like pandas, NumPy, and SciPy. The charts below are generated with the library called plotly].

We proceeded as such:

Step 1: Data Extraction and Preprocessing

Step 2: Update Frequency Analysis

Step 3: Standard Deviation Analysis

Step 4: Results analysis

Extraction & Preprocessing

The goal of preprocessing is to clean the data as much as possible to produce a reliable analysis. The preprocessing step includes mask by dates that we chose based on reliability, extending missing values, and filtering the outliers. Extending uses historical data and interpolation – the outlier filter simply ignores values above the threshold with standard deviation (std).

Market Frequency Analysis

Most of the forward markets are more active than the spot markets. From the 22 markets we analyze, there are 18 markets with forward price update frequencies that are at least twice as more frequently updated than spot prices. That is understandable because the spot markets are in narrower windows than the forward ones. Nevertheless, some prices stick out in the spot market as more active than the forward market (like Russia Milling Wheat 13.5 FOB Russia, or Romania Milling Wheat FOB Bulgaria).

We aim to then compare spot and forward update frequencies in the different markets. The frequency is the count of updates for spot prices or forward prices in a month. As such, it is an indicator of market volumes and activity.

Active forward prices & Stable spot prices

Most of the forward markets are more active than the spot markets. From the 22 markets we analyze, there are 18 markets with forward price update frequencies that are at least twice as more frequently updated than spot prices. That is understandable because the spot markets are in narrower windows than the forward ones. Nevertheless, some prices stick out in the spot market as more active than the forward market (like Russia Milling Wheat 13.5 FOB Russia, or Romania Milling Wheat FOB Bulgaria).

We aim to then compare spot and forward update frequencies in the different markets. The frequency is the count of updates for spot prices or forward prices in a month. As such, it is an indicator of market volumes and activity.

Figure 1: Cash Market prices with stable spot update frequencies and active forward frequencies, France Corn FOB France and Brazil Soybean FOB Brazil

We see that In this situation, spot prices are stable most of the year, but also that the forward update frequencies form wave-like patterns. They decrease or increase in periods of about 6 to 8 months. This is very frequent. Aside from one market, the remaining 21 forward markets have prices with higher variance in update frequency than for spot prices overall. However, we can observe that in this case, the frequency volume over time has decreased threefold. This trend is also observed in other markets like Ukraine Corn FOB Ukraine. Now, this is not always the case. In the case of Brazil Soybean FOB Brazil, the frequency volume increases with each new period.

Receding forward prices

In other scenarios, the forward price update frequencies show different patterns that are proper to them, but they all end up having their volumes crashing and slowly dying out.

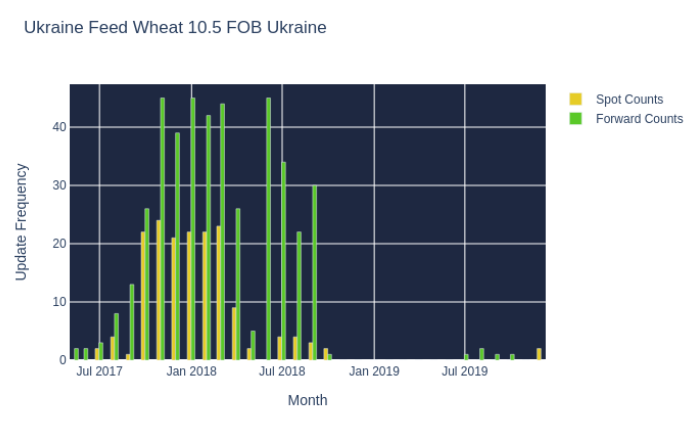

Figure 2: Cash Market Prices with receding forward prices update frequencies, Romania FOB Corn Bulgaria and Ukraine Feed Barley FOB Ukraine

In both cases, it is striking that the forward price frequency volume collapses around the same period. We can assume that this is due to an event related to the origin or maybe to this specific period in time. Nonetheless, each market has different characteristics, features, and dynamics.

We see that for Ukraine Feed Barley FOB Ukraine, there is an important seasonality. The volumes for both forward and spot begin increasing from January and peak in July, at which point it decreases until it reaches January. Moreover, January spot prices are historically more active than the forward market even though the forward market is active overall. For Ukraine Feed Wheat 10.5 FOB Ukraine however, there is no clear seasonality. This supports the idea that this recession is probably due to other factors.

Both markets lost their characteristics in late 2018 or early 2019 and weren’t able to reproduce this pattern and trading volume size – in certain periods, the forward updates disappear altogether. The silver lining, however, is that this does not necessarily mean that the market cannot recover. As we can see there are encouraging signs for Ukraine Feed Barley in 2020. Besides, even if spot price updates have receded, the volumes are still sizeable in their markets.

Standard Variation Analysis

The standard deviation represents the volatility of the prices. In general, high volatility prices are riskier than low volatility prices because the price is expected to be less predictable.

The variance dynamics are different from market to market. Hence we look at how the variance behaves in different markets.

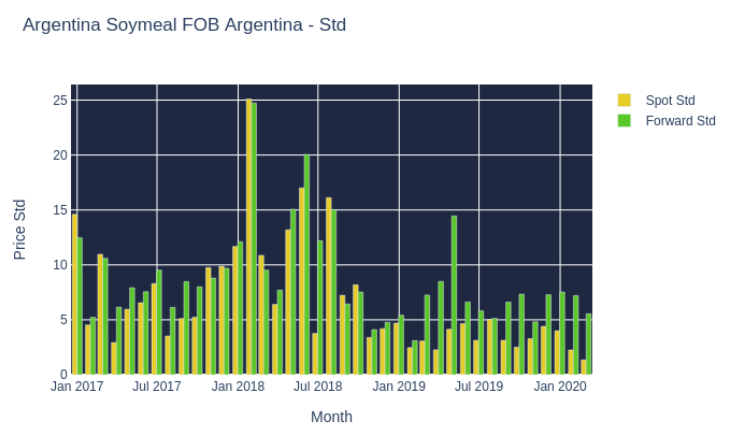

Figure 3: Price Standard Deviation along time, Argentina Soymeal FOB Argentina and France Barley FOB France

We see that in Argentina Soymeal FOB Argentina follows the general rule and has stable spot prices update frequencies and active forward frequencies. But when we inspect the standard deviation chart we see that spot prices are as volatile as the forward prices. This is despite them having less volume and a strict window. Additionally, we can spot that volatility can be seasonal. Looking at the France Feed Barley FOB France market, variations follow a wave-like pattern. We observe the standard deviation peaks around July from 2017 onward indicating seasonality for the volatility of the price. This also corresponds to an important time of the year for the market. Therefore we understand that for this market specifically, the volatility is linked to the activity of the market.

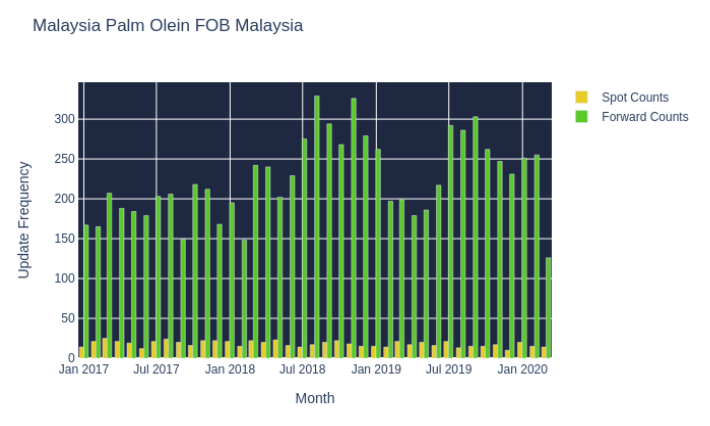

Nevertheless, we don’t see this kind of pattern for characteristics in some markets. In the Malaysia Palm Olein FOB Malaysia market, the price variation is peaking in February 2017 but in the following years, the maximum variations are around November in 2018 and July in 2019. This highlights the lack of pattern for seasonality.

Figure 4: Comparison between the standard deviation and update frequency for Malaysia Palm Olein FOB Malaysia from Jan 2017 to March 2020

Moreover, comparing the price variations to the update frequencies (figure 4), we can observe that the price variation patterns are not similar to the update frequency ones. In most cases, there is no correlation between both. Hence, for the Malaysia Palm Olein FOB Malaysia market, we see that the price variations are independent of the update frequency of spot and forward prices.

Conclusion

From the study and results, we can make some insightful conclusions. However, it is important to consider that they are only as valuable as AgFlow’s environment reach for contributors’ data. These results could potentially variate with additional contributors.

We saw that most markets have a stable spot price update frequency and high update frequency for the forward prices, and thus a very active forward activity trading mostly forward. However, some markets are very active on a spot basis. For example, we identified Romania – Bulgaria, or Russia Milling Wheat to be trading mostly spot, whilst Ukraine Milling Wheat is trading forward.

Also, we identified that markets can lose their features and change their dynamics. For example, a market maintains the forward update frequency volume high for a certain period, but then loses its forward volume and can become a spot-based structure. This is what happened to the Romania- Bulgaria Corn FOB market when it lost its volume in April 2018.

Whilst spot price update frequency is relatively stable for most markets, we also spotted seasonality patterns in forward price update frequency volumes. This feature is present in many markets throughout the study – for example, in Brazil Soybean FOB Brazil, Indonesia Palm Oil FOB Indonesia, or France Corn FOB France. Furthermore, this seasonality can also be observed for both spot and forward prices in some markets showing that these are specifically driven by seasonality. Some other markets also show a recession – for instance, Russia Milling Wheat 11.5 FOB Russia – as both its spot and forward update frequency volume decreased from January 2018 to September 2019.

Studying volatility with the standard deviation graphs, we highlighted that volatility can be affected by seasonality and thus the trading risk can depend on the period of the trade for both spot and forward prices. This is what we observed in the France Feed Barley FOB France market. Moreover, although spot prices have a stable and low update frequency volume, they can be more volatile than forward prices and therefore display no correlation between price update frequencies and price volatility. Furthermore, we saw that volatility can also be independent of seasonality, just like in the Malaysia Palm Olein FOB Malaysia market.

Finally, we can conclude that cash market frequencies are driven by different aspects. While seasonality is a big factor in most markets, the proper trading dynamics of a market (i.e trade forward more than spot) also influence the update frequency and the volumes of prices. There are also aspects outside of the scope of this study that can influence the markets’ frequencies and provoke recessions and dynamics changes. Volatility is also important in the cash markets. We saw that it was also driven by seasonality most of the time but also that it could be independent of quotes’ price frequencies. Nonetheless, the forward prices have a larger variation in general, and although they can present higher risks, they can also yield higher rewards. This could be one of the reasons why markets are leaning more towards Forward than Spot prices. And hence why most markets have higher forward frequencies than spot ones.